Moody’s expects property/casualty commercial insurance rate hikes to continue for the balance of the year, making 2013 the third straight full year of rising rates for commercial lines carriers, according to a special comment published Aug. 26.

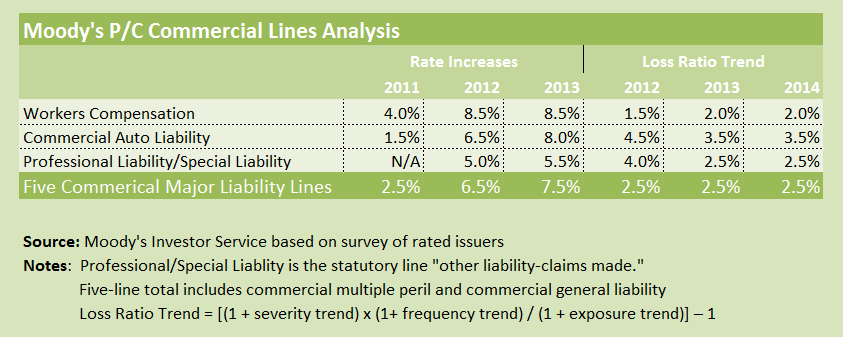

Referring to survey data collected from rated issuers for the workers’ compensation, commercial general liability, professional liability, commercial auto and commercial multiple peril lines, Moody’s reported that commercial insurers are expecting average rate increases of roughly 7.5 percent for policies written in 2013, up from 6.5 percent for 2012 and 2.5 percent in 2011.

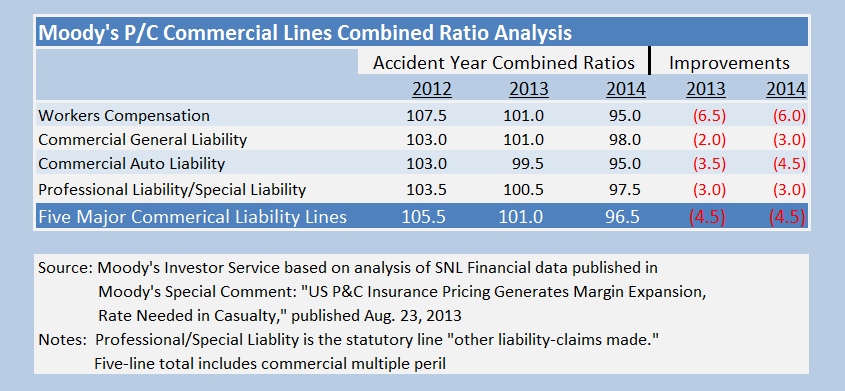

Given the current level of price increases, which are outpacing loss ratio trends, Moody’s forecasts that underwriting margins will also continue to improve, with the industry aggregate commercial lines combined ratio falling to 101 for 2013 and down to 96.5 for 2014. Both figures are substantially better than the 105.5 Moody’s calculated for 2012 based on SNL Financial data.

According to the report authored by Moody’s analyst Jasper Cooper, surveyed companies expect accident-year loss ratio trends to continue at about 2.5 percent in 2013 and 2014 — a level similar to 2012.

Workers’ Comp Analysis

Particularly striking among Moody’s line-by-line analysis of the combined ratio impacts of price changes relative to loss ratio trends is the degree of improvement indicated for the workers’ comp line. For workers’ comp, Moody’s estimates an accident-year 2013 combined ratio coming in just a point above break-even, at 101, compared to 107.5 for 2012 and 118 as recently as 2010. For 2014, Moody’s is projecting an accident-year combined ratio of 95 for the line.

While combined ratios are improving, Moody’s reveals that a number of workers’ comp carriers are signaling “a moderate decline in risk appetite” for 2013. The Moody’s report suggests that this reduced appetite will push further pricing improvements in 2014 but notes that the appetite decline is not as pronounced as it was during the early part of the last decade.

Operating returns-on-surplus for workers’ comp are still low relative to target returns, and further rate increases are needed given the line’s sensitivity to low new-money rates and lower reserve releases on older accident years, Moody’s says.

Moody’s estimates that a 101 combined ratio for workers’ comp for accident-year 2013 would result in a pre-tax operating return-on-surplus of about 8.5 percent (assuming a 3 percent investment yield), while a 95 combined ratio for accident-year 2014 would result in a pre-tax operating return-on-surplus of about 12 percent.

What If Pricing Falls

The report, which includes a similar analysis for each of the five major commercial insurance lines, also provides indications of where combined ratios and returns-on-surplus will fall at different prospective investment yield levels and if insurance pricing improvements don’t persist into 2014.

For workers’ comp, for example, Moody’s believes that impact of each percentage-point increase in investment yield on operating returns is equivalent to about a 5.5-point decrease in the combined ratio.

In addition, a 12 percent return-on-surplus — predicted for 2014 assuming a 3 percent investment yield — would jump to 15 percent if the yield is 4 percent and fall to 10 percent for a yield of 2.5 percent.

Further, if price increases were to stop in 2014, the accident-year 2014 combined ratio for workers’ comp could come in at 99 rather than the 95 that Moody’s is forecasting under a scenario of continued price improvements.

Topics Profit Loss Commercial Lines Excess Surplus Workers' Compensation Business Insurance Pricing Trends

Was this article valuable?

Here are more articles you may enjoy.

Berry Producer Driscoll’s Sued Over Alleged Greenwashing, Use of Forever Chemicals

Berry Producer Driscoll’s Sued Over Alleged Greenwashing, Use of Forever Chemicals  Bill to Curb Staged Accidents Introduced in Senate

Bill to Curb Staged Accidents Introduced in Senate  Viewpoint: Who Gets Credit for Successful Renewal During Soft Reinsurance Market?

Viewpoint: Who Gets Credit for Successful Renewal During Soft Reinsurance Market?  After 55 Years in Florida Insurance, Tom Lynch Reflects on Agencies, Changes Needed

After 55 Years in Florida Insurance, Tom Lynch Reflects on Agencies, Changes Needed

From This Issue