Specializing is one way to get ahead in today’s insurance world. But becoming an expert comes with its own share of risks.

Phrases such as “expert” or “specialist” have the potential to raise the level of legal liability for agencies, according to Curtis Pearsall, president of Pearsall Associates Inc., a risk management consulting firm and a special consultant to the Utica National Agents Errors and Omissions (E&O) program.

“Typically, an agent is an order taker. They provide or are asked to provide the coverage that the customer is looking for. If they are an expert or a specialist, it then potentially takes their level of legal liability up to the standard of an advisor,” Pearsall said.

For example, if an agency says that it is a specialist in writing restaurants, and all of a sudden the restaurant does not have any liquor liability coverage, then the agent could potentially be held to a higher standard because the agency indicated that it specializes in that class of business and really knows the exposures of that class of business, Pearsall said.

“The words that you use in promoting your agency, whether it’s on the website, whether it’s in your proposals, wherever, if you’re using the word ‘expert’ or ‘specialist,’ they have the potential to raise the standard of legal liability,” Pearsall said.

While specialists have the expertise needed to reduce E&O exposures, specialization also brings the potential for higher claims settlements should an E&O situation arise, according to Sabrena Sally, head of Swiss Re Corporate Solution’s U.S. Agents E&O program.

From an E&O perspective, there are two schools of thought. “One is that, if you’re a specialist, you certainly have more expertise and knowledge to bring to the table than someone, for example, who writes only a few aircrafts [specialty risk] per year. Someone that specializes in aviation has the relationships with the carrier. They have expert producers and CSRs [customer service representatives], and are much less likely to have a claim.”

At the same time, some specializations – not all, but some – bring with them the potential for catastrophic claim settlements, Sally said.

Gary Mann, director, professional liability, for Fireman’s Fund Insurance Co., agrees that specialization can be dangerous to agency E&O, with the type of specialty also being a consideration.

“It can be a double-edged sword,” Mann said. “What matters most is the type of specialization. With a specialist agency, the agency is better managed, has a better grasp of coverages and the market,” he said. However, in a specialty industry the insureds tend to be more sophisticated as well, which raises the bar for agents.

Also, agencies that specialize in one industry can have an aggregation of risks from an E&O standpoint, Mann says. “So a single loss can affect to a much greater degree.”

While being an expert increases an agency’s E&O risk, misrepresenting expertise is even riskier.

“There is danger in dabbling,” says David Hulcher, assistant vice president of agency professional liability risk management for the Independent Agents & Brokers of America (Big “I”). “Agents always need to know themselves and make sure they understand their area of knowledge and experience.”

Hulcher, who helps agencies in the Big “I’s” Professional Liability Program avoid claims by offering tools and risk management tips, advises agencies to proceed with caution in a new business opportunity if they’re not comfortable and lack experience or product knowledge in that industry.

“Agents need to be aware that if they don’t have that expertise, consider walking away from the account or consider working with another agent or a wholesaler that has that expertise … because there is danger in dabbling if you don’t understand either the process or the coverage that you’re selling,” Hulcher says.

Standard of care is an important topic for agents, Hulcher says. The standard of care is the degree of prudence and caution required when rendering services to customers. Swiss Re and the Big “I” Professional Liability Program recently offered a free webinar on the subject, titled “Understanding Your Standard of Care” to address the issue. (http://rms.iiaba.net/Content/Publications-Media/Webinars/Webinars.aspx)

Both Swiss Re Corporate Solutions and Fireman’s Fund serve as underwriting carriers for the Big “I’s” Professional Liability Program.

“We spend a lot of time discussing an agent’s standard of care, which varies by the state in which they’re licensed and selling insurance, and statements made as to one’s expertise or specialization can serve to increase the standard of care beyond their legal duty,” Sally said. According to the Swiss Re webinar, the trend among states is toward a higher standard of care that includes an obligation to advise insureds about additional coverages and limits There are very few order taker states, so playing to the higher standard better serves both agents and clients.

Buyer Beware

Buying agency E&O coverage can also present dangers, especially when agency owners don’t understand the difference in coverage provided by various agency E&O markets.

“There are substantial differences in the coverages being offered by E&O providers as it’s always been,” said Ron Von Haden, executive vice president and CEO of PIA National, which offers its members an agency E&O product called PIA Pro underwritten by Argonaut-Midwest Insurance Co.

“As with any type of insurance if you buy a stripped down policy you would expect to pay less for it and that’s no different in the E&O market,” Von Haden said. “I’ve seen policies being offered for considerably less than the major players in the market that have the better forms. A stripped down policy is a stripped down price.”

It’s important for agents to compare policy forms before moving their agency’s E&O coverage, Pearsall said.

“One thing about errors and omissions is that no two policies are the same,” he said.

“They must do some type of a comparison, or ask the agents’ association or the wholesaler, or whoever they’re interacting with, ‘What are some of the differences?’ Sometimes, some of those carriers will provide checklists of what things to look at, things such as whether its claims made, claims made and reported … two different concepts that agents need to be aware of … in terms of what their responsibility is – deductibles, definition of who is an insured, what professional services are covered, what are the tail options.”

There’s a host of differences to consider when shopping agency E&O. Pearsall recommends agents asking the potential E&O carrier for a specimen policy before moving coverage so they can review it, and make sure that they understand it.

“Because, if not, they could be moving their account to another carrier strictly based on price,” Pearsall said. “Sometimes, you get what you pay for.”

People – even some agents – look at insurance as a commodity, Hulcher said. But purchasing E&O coverage should not just be about price, he says.

“You need to think through other things when it comes to buying your E&O coverage. It’s not just about price. It’s about price, it’s about the product, and it’s about the claims support that you get, where the rubber meets the road, when the time comes that you’ve had somebody that’s brought an E&O claim against you, and how that claim is handled.”

Hulcher agrees there’s some danger in moving E&O carriers as well. “You’ve got to make sure you’re reviewing the product.

But not all Big “I” or PIA members buy their association’s professional liability program.

According to Hulcher, those agencies that don’t buy coverage through the Big “I” Professional Liability Program are likely looking for a better price. “The reality is, you could potentially go out and get a better price, but this program is not just about price,” Hulcher said. “But at the end of the day the Big ‘I’ Professional Liability Program is the largest program in the country. We understand where the losses are coming from, and we think we can give a good long-term, stable price that’s going to offer you consistency over time.”

Fireman’s Fund has been an underwriting insurer for the Big “I” program since 2006. According to Mann, an agency might fall outside of an association program because of its operations and size, or even its specialization.

Some agencies may choose agency E&O coverage through a non-admitted market instead of an admitted market.

Mark Harris, president and CEO of Quadrant Insurance Managers and Epoch Underwriting Management, says that the size of the agency matters when searching for the right agency E&O market. Quadrant offers retail insurance agent E&O insurance nationwide through multiple A-rated surplus lines markets.

“When agencies get bigger and more complex, a lot of the admitted markets cannot accommodate the growth-generated exposures,” he says. That’s when the surplus lines market becomes a very viable option for agencies since these insurers have flexibility to amend their rates and forms.

For example, an agency might go to a surplus lines market for E&O coverage rather than an admitted market if that agency has employees working as registered reps.

“Let’s say I’m a retail agency and I have some people with series 6 and 7 licenses, and they want to become client investment advisors. Most agency E&O policies aren’t written to do that. The reason: insurance agents E&O policies are pitched to the exposures of the insurance profession. Registered reps are more like securities dealers. Most agents or brokers E&O policies don’t contain the exclusions necessary for that exposure. I’m not saying that some admitted markets couldn’t make adjustments; some will and some won’t.”

Market Conditions

For 2013, the industry saw a few carriers either withdraw from the agency E&O market or limit their underwriting appetite, according to Swiss Re’s Sally. But all the experts agree that in general, the agency E&O market still seems to have ample capacity and availability.

“For newer agencies, or brand new startups … those agencies typically have to access the non-admitted market, but there still is an underwriting appetite for those,” Sally said.

“Right now the markets are pretty wide open,” said PIA’s Von Haden. “I’m not noticing any difficulties in the majority of agents being able to secure coverage from a multitude of markets, particularly the ones that have been stable for years.”

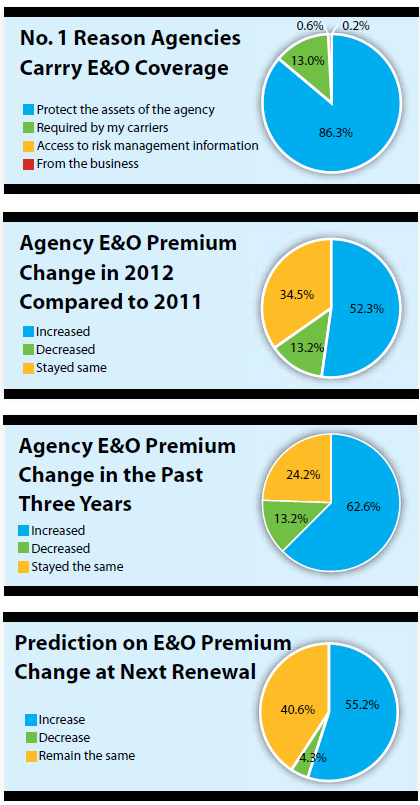

Despite widespread availability, agency E&O prices are on the rise. According to Insurance Journal’s 2013 Agency E&O Survey, 52.3 percent of agencies saw E&O premiums increase in 2012 compared to 2011, and 55.2 percent expect E&O premiums to increase again at the next renewal.

The exclusive IJ survey is based on responses from 684 agency owners across the country from Oct. 6-21, 2013.

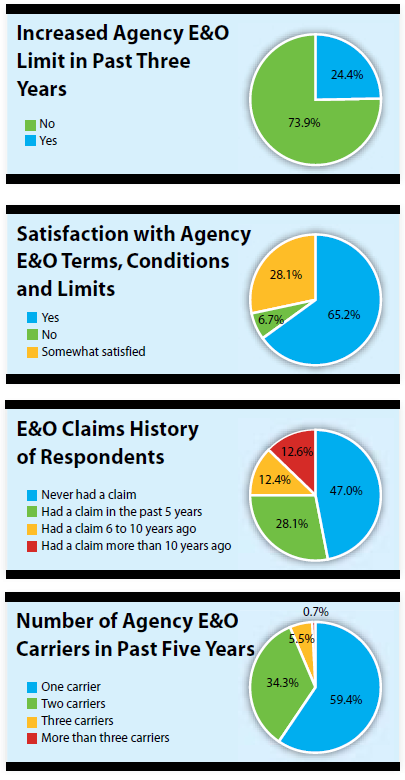

Even though prices are on the rise, most agencies (65.2 percent) purchasing E&O coverage say they are satisfied with E&O terms, conditions and limits today, according to the survey.

For clean risks, Pearsall sees agency E&O increasing about 3 to 5 percent on average. However for agencies that have had a claim or two, prices have jumped more and those agencies probably are seeing different terms and higher deductibles, he said.

“This is the time that the E&O carriers try to react to the hard market, and maybe try to get some additional pricing because, they know, at some point in time, it’s going to turn the other way again,” Pearsall said.

While most agencies stick with their E&O carrier, some agencies do shop around. According to Insurance Journal’s 2013 survey, 59.4 percent of agencies have had the same E&O carrier for at least the past five years, and 34.3 percent have had two carriers in the past five years. However, of those that shopped E&O markets, 29.4 percent said the reason they shopped was for a lower price.

Claims

When it comes to claims in agency E&O, the same issue continues to crop up. The failure to provide the proper coverage continues to top the list as the leading claim in agency E&O.

The poor economy did lead to a few unique claims trends, according to Swiss Re’s Sally.

“We certainly saw agency customers that were lowering coverages to save money. That can lead later to allegations of forgetful memories when a claim comes around and there’s less coverage in place than the agency customer would have needed.”

Insurers also saw E&O issues pop up with home vacancies in recent years. “So many homes became vacant throughout the country. It became a trend for opportunistic thieves, and then we saw issues of uncovered claims. The insurance carrier was not aware of the vacancy and that caused some allegations against agents,” Sally said.

Other trends in agency E&O continue to evolve, Pearsall said.

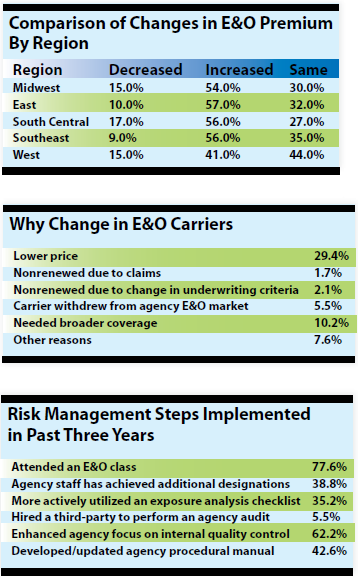

“Certainly, certificates continue to be a concern for most carriers. They’re indicating somewhere around 5 percent to 8 percent of E&O claims involve a certificate.”

Weather-related catastrophes continue to put stress on agency E&O claims.

“Superstorm Sandy generated a tremendous amount of E&O activity. Obviously, a lot of flood issues, but also a lot of business interruption claims, as a result of businesses not having any business interruption coverage,” Pearsall said.

Even with Sandy, E&O claim frequency is stable, according to Pearsall. “It’s pretty much still in really good shape.”

That could change with the implementation of the Affordable Care Act.

“We think about how healthcare reform will impact E&O a lot, almost on a daily basis,” said Sally. “There’s just uncertainty around the type of roles that agents may assume, as the distribution of healthcare changes and they find their way to offering different types of services to customers. We try to think ahead on what types of liability that may create for an agency. … There’s no answer yet because it’s completely new territory.”

Quadrant Insurance’s Harris says, “The reality is nobody knows; it’s all conjecture at this point.” One thing is certain, he says, as healthcare continues to evolve, agency E&O and the insurance industry are going to have to evolve with it.

Insurance Journal wishes to thank Demotech Inc. for providing analysis once again for this year’s Agency E&O Survey.

Was this article valuable?

Here are more articles you may enjoy.

Walmart Removes Four Taylor Farms Salads as Recalls Spread

Walmart Removes Four Taylor Farms Salads as Recalls Spread  Farmers Looks to Make it Easier for Consumers to Understand Insurance

Farmers Looks to Make it Easier for Consumers to Understand Insurance  One Weather Firm Warns New England Could See Big Hurricane This Season

One Weather Firm Warns New England Could See Big Hurricane This Season  Iran Renews Attacks on Gulf States After Another Night of US Strikes

Iran Renews Attacks on Gulf States After Another Night of US Strikes

From This Issue