Fires across North America in 2018 have continued the pattern of extreme destruction established by significant insured loss events in both Northern and Southern California last year and the 2016 disasters in Alberta and Tennessee. These events have driven the insurance industry – residential insurance carriers in particular – to re-evaluate its wildfire risk management practices and investigate new technologies to aid in that effort.

With new or updated catastrophe models and hazard scoring tools coming to market this year, as well as revamped internal inspection processes, insurers have the opportunity to take a considerable step forward in understanding their wildfire risk and the factors that differentiate individual structures. Meanwhile, high-quality aerial imagery from satellites and aircraft has become widely available but remains challenging to analyze and use at scale.

To drive forward progress, technologies such as artificial intelligence and computer vision can unlock previously unavailable property information from imagery and feed the catastrophe models and data analytics which enable more granular underwriting and risk mitigation efforts.

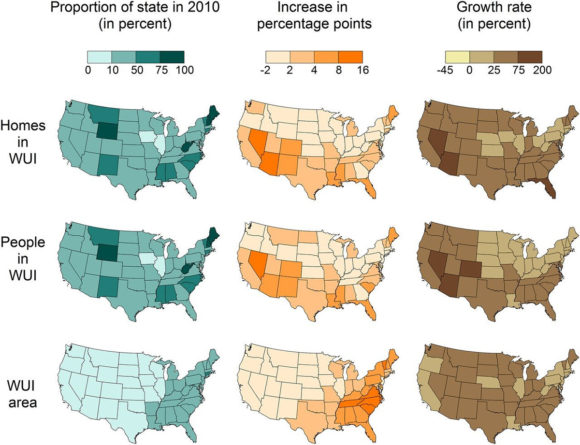

Such progress in this space is badly needed. This year’s wildfires have climbed into the lists of the most destructive, largest or deadliest events across the U.S. and California in particular. Many of these lists are now filled with events from 2017 or 2018, including the recent, heart-rending tragedy in Paradise, Calif., which was devastated by the Camp Fire, the most destructive fire in U.S. history and deadliest in over a century. The changing conditions on the ground, such as the rapid growth of exposure in the wildland-urban interface (WUI), that have resulted in this heightened level of destructive wildfires are being carefully watched across the insurance industry and government sector.

A recent article published in the Proceedings of the National Academy of Science (PNAS) stated that “the WUI in the United States grew rapidly from 1990 to 2010 in terms of both number of new houses (from 30.8 to 43.4 million; 41 percent growth) and land area (from 581,000 to 770,000 km2; 33 percent growth), making it the fastest-growing land use type in the conterminous United States.”

In January 2018, the California Department of Insurance (CDI) released a report that highlights issues with existing wildfire risk quantification tools, suggesting they “are not accurate, do not provide satellite imagery that is granular enough to objectively identify fuel sources and other physical characteristics, and do not take into account mitigation done by the homeowner or community.” The report described their review of the risk models and pinpointed that individual homeowner or community mitigation efforts like vegetation clearance are not considered, in addition to consideration for differences in access.

Now, the focus is turning to technology solutions that better quantify this risk across the wildfire-urban interface.

New modeling tools, in particular those from the major catastrophe modeling vendors that can incorporate building-specific defensible space information, are being delivered across the insurance industry. However, to utilize these new tools, insurers need access to high-fidelity vegetation clearance data across the exposure in their books. As called out by the CDI report, granular aerial imagery is a key component of this effort.

Artificial intelligence (AI) and computer vision technologies are the missing link in converting such visual imagery into information that can be objectively captured and used. Paired with AI, computer vision obtains actionable information from images through detection and identification of patterns or objects. This is typically done by training convolutional neural networks (CNNs) on large image datasets. This technology stack has been used across several industries, such as industrial robot control, navigation for autonomous vehicles, and medical image processing. In insurance, AI has enabled several advances in areas like driver performance monitoring, claims management through chatbots, and underwriting insights. Now, AI and computer vision can be used to provide wildfire-relevant data, such as defensible space, on a massive scale.

For example, technology to derive property intelligence information can be used at the point of underwriting or for downstream portfolio management activities, like catastrophe modeling. Attributes, such as roof condition, roof covering or tree overhang, are detected and delivered using automated aerial imagery analysis across the continental United States, with nothing more than an address. This enables insurance carriers to put less of an emphasis on data capture by the customer or agent, while still having the most impactful information available instantly to make granular decisions about a property’s risk.

Focusing on wildfire risk, imagine defensible space information delivered as structured data for every property directly into carrier underwriting systems, rather than from inconsistent onsite inspections or time-consuming manual review of imagery. This information could identify if significant vegetation, such as dense trees or shrubs, are next to the structure or even overhanging it.

Automated systems could see if a clear space for defense has been maintained to keep the structure safe if a wildfire approaches the property. They may also be able to provide information on roof covering material (i.e. wood shingle), a key rating factor in wildfire-prone areas. These could be critical pieces of information that feed directly into the quantification of risk for a structure and need to be available at the point of underwriting. Property intelligence derived from AI and computer vision, used in tandem with the next generation of risk modeling tools, has the opportunity to make decisions about wildfire risk much more granular.

As wildfire risk continues to rise with increasing exposure throughout the wildland-urban interface, insurers will be challenged to have a better understanding of the locations they are underwriting and the portfolios being managed. Solutions must center on simplifying the workflows to gather and take action on property intelligence in a way that differentiates high-risk exposures. The industry stakeholders that leverage these new technologies will continue to have an advantage for understanding and acting upon this rapidly emerging catastrophic risk, could save billions of dollars in losses, and help homeowners protect their property before it’s too late.

Topics InsurTech USA Data Driven Artificial Intelligence California Catastrophe Natural Disasters Wildfire Underwriting Property Market Drones

Was this article valuable?

Here are more articles you may enjoy.

2,900 Required Condo Inspections Were Never Completed, Florida Report Finds

2,900 Required Condo Inspections Were Never Completed, Florida Report Finds  Can Reinsurers Maintain Underwriting Discipline or Will ‘Irrational’ Competition Return?

Can Reinsurers Maintain Underwriting Discipline or Will ‘Irrational’ Competition Return?  Zurich Insurance Earnings Boosted by Global Data Center Demand

Zurich Insurance Earnings Boosted by Global Data Center Demand

From This Issue