The year of 2018 brought an all-time high of merger and acquisition (M&A) activity to the insurance industry.

Consolidation of firms, both at a local level with M&A by independent agents and brokers, and acquisitions by larger, publicly-traded and privately-held firms, outpaced all prior years on record through the fourth quarter of 2018. While the economy started to see some headwinds with interest rate hikes and a shaky stock market performance in late 2018, valuation and deal activity around independently-held insurance firms held strong.

The insurance distribution industry is truly a gem in the eye of an investor. Many insurance distribution firms are capable of high levels of profitability, high rates of recurring revenue, and low requirements for capital expenditures and reinvestment. That’s why interest for acquisitions in this marketplace continues at a high rate. Combined with the overwhelmingly baby boomer ownership demographic and the lack of internal perpetuation plans in place at many firms, and you have the most active M&A market this industry has ever seen.

Another Record M&A Year

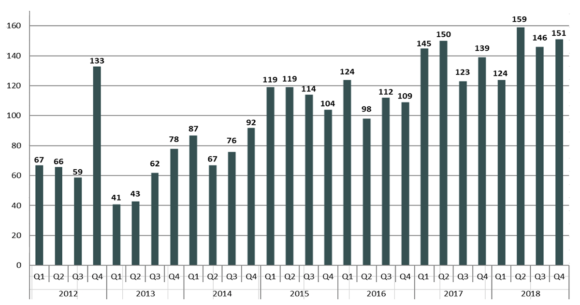

While some 2018 announcements trickle in late, we have the total number of announced 2018 transactions at 580, up from 557 in 2017. For half of the top 10 buyers in 2018, the fourth quarter was the busiest, in terms of the number of deal closings.

Larger, privately backed firms (mostly private equity-backed) continued to dominate the M&A activity and deal announcements in 2018, with roughly 60 percent of all deals.

Independent agents and brokers across the country, as buyers, closed and announced 20 percent of the total deals.

Publicly traded brokers closed 10 percent of the transactions. The remaining 10 percent of announced deals were completed by banks/thrifts (3 percent), insurance carriers (3 percent) and the remaining deals (4 percent) had other types of acquirers, such as private equity (PE) groups, underwriters, insurtech firms, specialty lenders, etc.

Top Buyers

The top buyer in 2018 was Acrisure LLC with 65 announced transactions. Acrisure is a PE backed firm, with investors including Blackstone Management Group, ABRY Partners, Veronis Suhler Stevenson, and Genstar Capital.

BroadStreet Partners Inc. was the second most active with 37 announced transactions. BroadStreet’s primary investors are Ontario Teachers’ Pension Plan and Century Equity Partners.

AssuredPartners, backed by Apax Partners, closed 34 deals in 2018, as did Alera Group, backed by Genstar Capital.

Arthur J. Gallagher & Co., a publicly traded firm, rounded out the top five, with 30 announced closed transactions. These top five firms completed slightly more than one-third of all announced transactions in 2018. Most of these firms were also in the top five of buyers in 2017, indicating that their voracious appetite for insurance firm acquisitions has continued.

The next five, to round out the top 10, were Hub International Limited (PE backed) with 28 transactions, Brown & Brown Inc. (publicly traded) with 24 deals, NFP Corp. (PE backed) with 18 deals, Seeman Holtz Property and Casualty Inc. (PE backed) with 17 deals, and OneDigital Insurance (PE backed) with 16 deals.

In total, the top 10 acquirers of 2018 completed just over half of all the deals announced for 2018.

Move to National

The acquired firms (the sellers) were located across the country, but nearly half of deals occurred with agencies located in California, Texas, Florida, Massachusetts, and New York. This isn’t surprising given the population and number of firms in those states.

Acquirers are aggressively seeking to build out their organizations across the country. While many began with a regional approach, most have moved to a national reach and are now making acquisitions across the country from New York to California to Florida.

In 2018, 53 percent of the seller firms were property/casualty insurance agency/brokerage firms, 22 percent were employee benefit focused firms, and 25 percent were multiline firms (writing both P/C and employee benefits). This trend held consistent with the percentages from 2017.

In addition, there does not appear to be any shift in the types of firms buyers are looking to acquire as their strategic/target acquisitions. They continue to focus on growing firms, with professional staff, infrastructure, proven profitability, a next generation of leadership and sales/producer talent. As 2018 wrapped up, the market showed no signs of a slowdown. Instead, there is a robust pipeline of deal activity underway for a busy start to 2019.

Was this article valuable?

Here are more articles you may enjoy.

A Chinese Spyware Tool Operates in 13 Countries, Cybersecurity Firm Says

A Chinese Spyware Tool Operates in 13 Countries, Cybersecurity Firm Says  Allstate Introduces Large Language Model, ALLIE

Allstate Introduces Large Language Model, ALLIE  American Family to Acquire Bowhead Specialty in $1.2B Cash Deal

American Family to Acquire Bowhead Specialty in $1.2B Cash Deal  Zurich Insurance Earnings Boosted by Global Data Center Demand

Zurich Insurance Earnings Boosted by Global Data Center Demand From This Issue