The shoe may eventually be placed on the other foot for the U.S.

This nation has a long-standing tradition of innovating products and ideas – particularly insurance products – and then exporting them to other countries.

Now the U.S. may benefit from an insurance-like product being developed for third-world countries to battle pandemics, which some experts think will be made more severe and widespread by climate change.

And that product, its designers say, may eventually create an entirely new market for private insurers and reinsurers in the U.S. and abroad.

Last month at the G7 Summit in Japan, participating countries agreed to support the implementation of the Pandemic Emergency Financing Facility.

This is a financial response mechanism to price pandemic risk under development by the World Bank in cooperation with the World Health Organization, global reinsurance companies and catastrophe modelers.

The idea is to facilitate the quick dispersal of funds in the event of large-scale disease outbreaks through this publicly-backed parametric product, which the World Bank will syndicate through capital markets, investors as well as insurance and reinsurance companies.

Just which insurers and reinsurers are so far involved has yet to be made public.

World Bank tapped Swiss Re and Munich Re to design the financing facility, and Boston, Mass.-based AIR Worldwide was brought in as the third-party modeler.

Financial Pillars

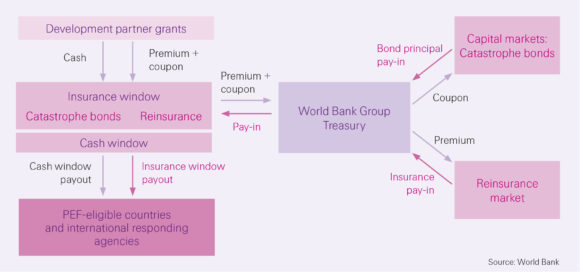

The PEF will enter into operation in late 2016, according to those involved. It will consist of two financing pillars: a parametric insurance mechanism, and a cash reserve composed of long-term pledges from development partners.

“The insurance mechanism is designed to facilitate quick, efficient outbreak response by providing funds to hire and deploy pre-approved international responders (response organizations, emergency task forces or national governments depending on existing response capacity) in affected countries to cover immediate objectives in the event of a major outbreak,” states a report released last week from students of the Johns Hopkins University School of Advanced International Studies.

The students collaborated with Swiss Re on the report to examine the implications of climate change on global pandemic risk, and to analyze the potential of the PEF to provide the basis for a long-term market for pandemic insurance. Swiss Re also helped fund the report.

Alex Kaplan, senior vice president of Swiss Re global partnerships, said the goal of the report – and the creation of the PEF to some extent – was to deal with a humanitarian and economic issue posed by both climate change and the threat of pandemics.

“You have two seemingly uncorrelated risks which are converging on a global scale and it’s something the industry and also the global community needs to be watching very closely,” Kaplan said.

The Johns Hopkins report draws a strong parallel between climate change and pandemics, citing two reports out this year: The Global Risk Report published by the World Economic Forum, which identifies a link between climate change and the spreading of infectious diseases; and the U.S Global Change Research Program report, which examines the various ways through which climate change will affect overall public health.

“Changes in climatic conditions will act as threat multipliers to a wide range of noncommunicable and infectious diseases, from temperature-related deaths, asthma and allergy conditions, water-related diseases such as cholera and meningitis, to mental health and stress-related illnesses,” the Johns Hopkins report states.

According to the report, climate change affects ecology and the vulnerability of human populations before an outbreak, and exacerbates the intensity during an outbreak.

Prior to an outbreak, changes in temperature, precipitation patterns and pH levels will affect the quantity and quality of ecosystem services – food supply, water availability – and supporting services like soil formation, and nutrient recycling. This impacts migratory patterns and the habitats of animals and insects, while changes in precipitation patterns, atmospheric temperature, and seasonality will influence animal and insect populations, according to the report.

The report also brings home the topics of climate change and pandemics for Americans who may think they’re immune to either: “The steady increase in temperatures in the Northeast and upper Midwest regions of the U.S. has contributed to the geographic expansion of tick habitat. Also, extended spring and summer periods and higher average temperatures lead to faster growth rates of mosquitoes, allows them more time to reproduce, and contributes to mosquito population growth.”

Mosquitoes aren’t just a nuisance. They transmit diseases like Zika, Dengue, Malaria, West Nile Fever and Yellow Fever, according to the report.

PEF Trigger

Under the PEF, payouts will be triggered when an outbreak meets a set of predetermined thresholds, such as death toll, or infections within a given timeframe, based on the characteristics of each of the covered diseases.

The initial phase of the program will cover filovirus, coronavirus (this includes SARS and MERS), ADOM, and pandemic influenza.

The humanitarian aspect behind the idea is clear. But how does the economy tie in to all of this?

The financial mechanism is designed to get funds into affected countries in as little as 10 days in contrast to the slow political decision-making processes of dispersing funds.

Take the Ebola virus outbreak for example.

Six months after the initial cases were reported, roughly one-third of financial pledges had been dispersed. As the crisis worsened, resource requirements grew, according to the report.

“Appeals for funds by the WHO grew from USD 4.8 million in early April 2014 at the onset of the outbreak to USD 1.5 billion by November of the same year, to roughly USD 4 billion by January 2015,” the report states. “Combined with a poorly coordinated global response and lack of capacity, this left Guinea, Liberia and Sierra Leone devastated both physically (lives lost) and economically.”

Nikhil da Victoria Lobo, head of global partnerships Americas for Swiss Re, said roughly $5.4 billion in appropriations came from the U.S. government following Ebola outbreak.

“It would be far smaller for the U.S. government to put up some tens of millions of dollars …than to appropriate $5.4 billion after the horse has left the barn,” Lobo said.

The ongoing Zika outbreak in Latin America has already begun to slow projected growth in the region, while response costs are mounting and governments and businesses are losing revenues. Zika has also been tied to babies being born with encephalitis.

“Zika creeps forward every week,” Lobo said, adding that it isn’t just a problem on foreign soil. Earlier this year a woman became New Jersey’s first confirmed case of Zika.

Premium Support

The first three-year phase the PEF (see graphic) entails G7 donor countries providing premium support to the World Bank, enabling the PEF to purchase insurance coverage on behalf of 77 developing countries to cover the costs of containing outbreaks.

This is expected to change pandemic financing by quantifying the risk, according to the report.

“By allocating capital to the risk of a pandemic outbreak, reinsurer and capital market investors will be effectively putting a price tag on the frequency and severity of pandemic outbreaks,” the report states. “Until now, responding to large outbreaks has been done on an ad hoc basis, with the WHO, affected countries and international organizations estimating the cost of the response as an outbreak progresses.”

Insurers and reinsurers may want to note that the PEF is expected to evolve to expand coverage and encourage private sector involvement in pandemic financing.

“We believe this is a very powerful opportunity to create a market … and also to introduce many of these large insurance and reinsurance companies to these markets,” Lobo said.

Not only does this lay the groundwork for the private industry to delve into parametric products at home and abroad, it puts companies in a position with both potential public and private entity customers to introduce to them other products that aren’t covered under the PEF, such as business interruption insurance and agricultural products, according to Lobo.

The initial phases of the PEF are expected to reduce the cost for other insurance companies and institutional investors who want to become involved in the market, and as a global insurance mechanism it will pool the outbreak risk from different regions, according to the report.

“The PEF will increase global demand for data on diseases and it will encourage further research and understanding into how to respond to pandemics and how factors like climate change affect the occurrence of disease outbreaks,” the report states. “The barriers to entry into the industry of pandemic risk will be greatly reduced by the trailblazing efforts of the PEF and its partners.”

As disease modeling improves over time, it will enable the insurance market to expand to cover a wider spread of outbreak risks, and in the long run the cost of insuring against pandemic risk is expected to fall. As the pool of covered countries expands, the premium costs will go down for all members.

“This has already proven true with other, sustainable types of sovereign risk mechanisms like the Caribbean Catastrophe Risk Insurance Facility (CCRIF) and the African Risk Capacity (ARC),” the report states.

Unlike the markets they often arise in, pandemics are not an emerging threat, and they aren’t confined by borders or wealth. That’s a reality U.S. insurers and residents alike should pay attention to.

“Pandemics are not an emerging problem, they are a humanity problem,” Lobo said. “And the solutions and needs that are required are as valid in the United States as they are in sub-Saharan Africa.”

Past columns:

- What University of Washington’s Climate Risk and Insurance Summit Has in Common with Paris

- Report Says Climate Change Could Make Some Wines Less Tasty

- Climate Change and The Conservative Republican

- Few Small Businesses Feel the Need to Prepare for Climate Change

- Climate Change Easy Bet to Be Hot Topic at Insurance Regulators’ Meeting

Pandemics in a Changing Climate

Topics USA Carriers Reinsurance Climate Change

Was this article valuable?

Here are more articles you may enjoy.

Brown & Brown Estimates Cost of Howden-Driven Talent War Could Hit $60M in 2026

Brown & Brown Estimates Cost of Howden-Driven Talent War Could Hit $60M in 2026  Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks

Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks  CBIZ Brokerage to Be Spun Off, Backed by Private Equity, After $5B Grant Thornton Deal

CBIZ Brokerage to Be Spun Off, Backed by Private Equity, After $5B Grant Thornton Deal