A handful of consumer and climate groups are calling on the insurance industry to ditch fossil fuels as part of a new campaign called Insure Our Future.

The entreaty came on the eve of this week’s Global Climate Action Summit, a three-day event in San Francisco, Calif., which drew a reported 4,000-plus delegates and included more than 500 climate commitments.

The Insure Our Future campaign calls out the U.S. insurance industry as a major contributor to climate change because it is a major investor in fossil fuel companies, reporting that the 40 largest U.S. insurers hold over $450 billion in coal, oil, gas and electric utility stocks and bonds.

The Property Casualty Insurers Association of America says people behind this campaign ignore that fact that insurers are obliged the make the safest, best investments with their money.

“Too often climate activist groups take a narrow view that reflects a superficial understanding of the problem that our nation faces and the proper role for insurance,” David Kodoma, PCI’s assistant vice president of research and policy analysis, said in a statement. “It is important to note that insurer investments are highly regulated and monitored by state insurance regulators and rating agencies. Additionally, insurers are actively engaged, implementing effective catastrophe risk management strategies and mitigation efforts that help policyholders and communities in every region prepare and prevent damage from extreme weather.”

The effort to get insurers to rid themselves of fossil fuel investments has been ongoing.

California Insurance Commissioner Dave Jones has often voiced his wish that insurers divest from coal. He established the Climate Risk Carbon Initiative, which includes information on the amount of oil, gas, coal and utilities investments held by insurance companies, and whether the insurers have divested from thermal coal, the amount of thermal coal divested and any future commitments to divest.

A number large insurers in Europe, have already begun to divest, according to the Sunrise Project, which reports that 17 large insurers have divested roughly $30 billion from coal companies since 2015.

The Insure Our Future campaign touts itself as “the first campaign focusing on the U.S. insurance industry’s significant role in perpetuating climate chaos.”

The campaign’s does favor one U.S. insurer – at least in terms of timing.

Insurtech Lemonade announced this week that it won’t invest in coal, stating that “insurance companies shouldn’t fund the very harms they’re meant to protect against.” The New York-based start-up called on other insurers to do the same.

According to the Insure Our Future campaign, which gave a shout out to Lemonde’s move in press materials, Lemonade is the first U.S. insurer to commit to never invest in fossil fuels.

Allianz

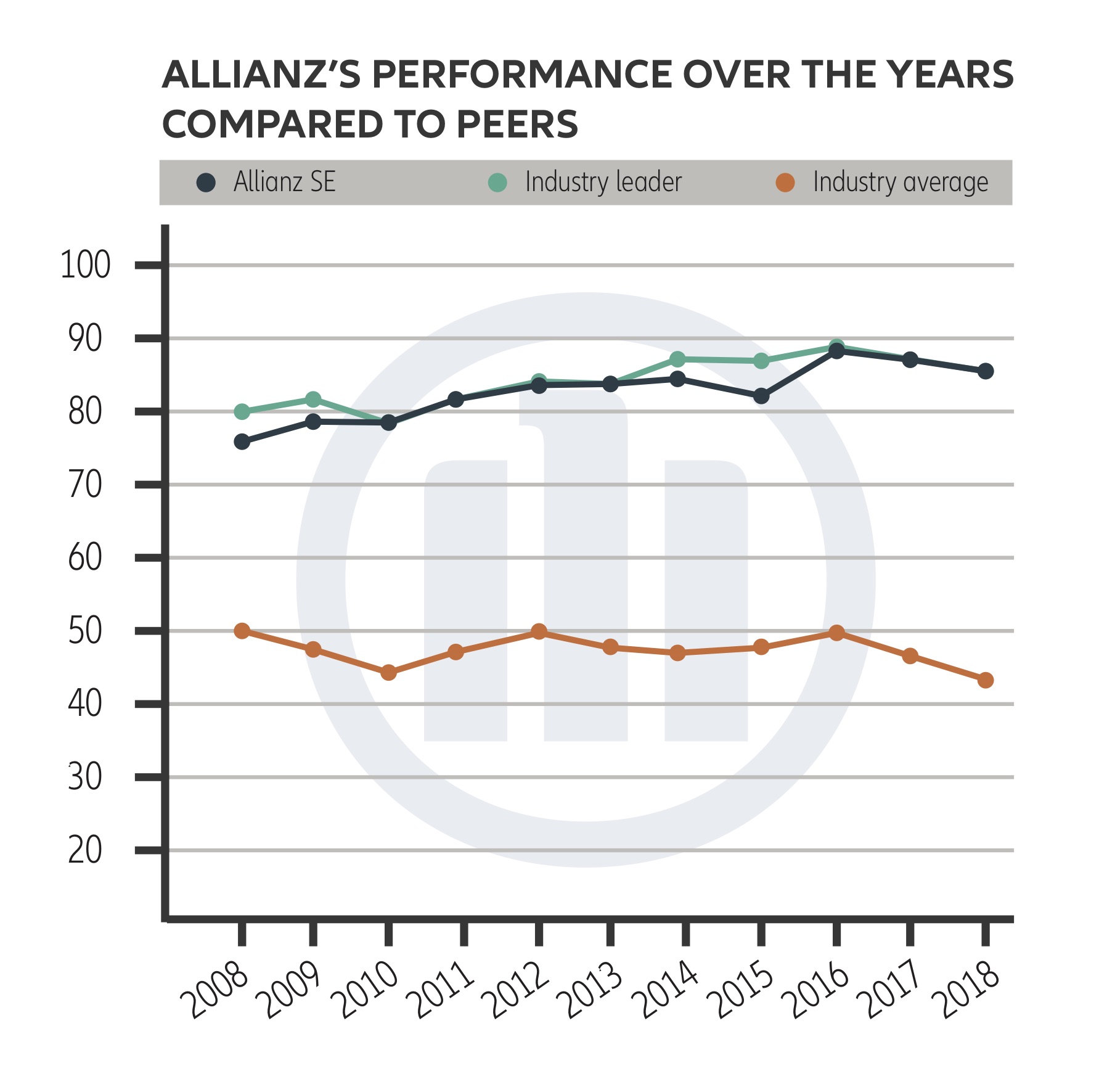

Allianz has topped the Dow Jones Sustainability Index 2018 as most the sustainable insurer. The company was named the insurance sector leader in the new DJSI, which was released this week.

Other sector leaders included Peugeot SA for automobiles, LG Electronics Inc. for consumer electronics, UBS Group AG for diversified financials and UnitedHealth Group Inc. for healthcare.

The DJSI, consider by some as “the gold standard for corporate sustainability,” tracks sustainability-driven companies based on RobecoSAM’s analysis of financially material environmental, social, and governance factors.

Allianz scored a sustainability rating of 85 out of 100 points for the second straight time. The median score for the insurance industry was 41.

Those doing the scoring assess companies on the basis of 80 to 120 industry-specific questions focusing on financially material economic, environmental and social factors that are relevant to companies’ success in an annual questionnaire sent to more than 3,500 of the world’s largest listed companies.

The company was named best in the sector in climate strategy, human capital development, information security, tax strategy and financial inclusion.

“We are very pleased with this result. It shows that our focus on ecological, social and governance criteria is being acknowledged by external sustainability experts,” Günther Thallinger, a member of the board of management of Allianz SE and responsible for investments and ESG, said in a statement.

According to Allianz, some of the company’s climate-friendly business operations and social engagement initiatives include:

- 165 insurance and financial products with ecological or social benefits

- 6 billion Euros ($6.55 billion) invested in renewable energies

- Reduction of the carbon footprint per employee by 17 percent

- Social engagement with around 80,000 hours of voluntary work by employees and 20 million Euros ($23.28 million) in donations

The Hartford was another big insurer named to the 2018 DJSI. It was the seventh year running that the Connecticut-based company has been named to the index.

“As a company in business for more than 200 years, we understand what it means to be sustainable,” Diane Cantello, head of corporate sustainability at The Hartford, said in a statement. “Our sustainability strategy is built around measurable goals that demonstrate our positive impact on the environment, our workforce, and the communities where we live and work.”

Investor Agenda

There was a flurry of initiatives and announcements at the Global Climate Action Summit.

The Investor Agenda launched on Wednesday during the summit. The Investor Agenda is intended to support investors in “accelerating and scaling-up the actions that are critical to tackling climate change and achieving the goals of the Paris Agreement,” those behind it say.

The initiative is designed to provide a way for investors to directly report actions they are taking and scale-up their commitment to act across four focus areas: investment, corporate engagement, investor disclosure and policy advocacy.

More than 392 investors with $32 trillion in assets collectively under management have already begun taking actions that are in line with the Investor Agenda, according to the group.

“Investors are showing great leadership to promote climate action in multiple fronts,” Patricia Espinosa, executive secretary of the United Nations Framework Convention on Climate Change, said during the climate summit. “Their efforts to meet the shortfall in the financial resources required to deliver the Paris Agreement goals, and further building on engagement with high-emitting sectors are a valuable contribution.”

The total number of investors taking action in line with The Investor Agenda is expected to grow over coming months and years.

Submissions will remain open for investors through The Investor Agenda website. Growing involvement of investors, will serve to increasingly reflect the full scale of momentum in global investor action on climate change.

Developed by seven founding partner organizations, and supported by 10 supporting partner organizations, the Investor Agenda brings together investor networks in Asia, Australia, Europe, and North America, and relevant supporting partner organizations.

The Investor Agenda has already received support from influential investors and climate figures alike, the group says.

The Guardian Vs. North Carolina

The Guardian and a handful of other media outlets are giving some play to a five-year-old North Carolina law in the wake of Hurricane Florence.

“In 2012, the state now in the path of Hurricane Florence reacted to a prediction by its Coastal Resources Commission that sea levels could rise by 39 inches over the next century by passing a law that banned policies based on such forecasts,” the article states.

Insurers are forecasting significant claims from businesses from Florence, which as of publication of this story was hitting the Southeast with fierce winds covering 15,000-plus square miles.

The Guardian article notes that North Carolina has a long, low-lying coastline and is considered to be vulnerable to rising sea levels. A report out in 2015 from the States at Risk project, which shows that Southeast states are unprepared for future risks from climate change, notes that North Carolina has 122,000 residents at risk of coastal flooding. By 2050, an additional 44,000 people are projected to be at risk due to sea level rise.

According to the Guardian story, dire predictions from the state’s coastal commission alarmed coastal developers and their allies, who said they did not believe the rise in sea level would be as bad as predicted and that such forecasts could unnecessarily hurt property values and drive up insurance costs.

State lawmakers quickly passed a law stating that these studies could not be used for forecasts because science wasn’t clear on the matter of climate change and that projections for rising sea levels could only be based on historical data.

“As a result, the state’s official policy, rather than adapting to the worst potential effects of climate change, has been to assume it simply won’t be that bad,” the Guardian article states. “Instead of forecasts, it has mandated predictions based on historical data on sea level rise.”

A report from North Carolina’s coastal commission issued after the law was passed looked just 30 years ahead and found that the rise in sea level during that time was likely to a more moderate 6 in. to 8 inches.

However, North Carolina could be turning around on some of its climate views. North Carolina Gov. Roy Cooper announced last year that state would join the U.S. Climate Alliance, a group of states pledged to reducing greenhouse gas emissions in line with the goals of the Paris climate accord.

Past columns:

- Report Outlines Climate Change Risks Faced by Insurance Sector

- San Francisco May Screen Insurers for Their Fossil Fuels Investments

- Survey Shows More Americans Believe There is ‘Solid Evidence’ of Global Warming

- Sea Level Rise Puts $117.5B at Risk from Chronic Flooding

- NOAA Expects Sea Level Rise to Produce Record Coastal Flooding This Year

Topics USA Carriers Energy Oil Gas North Carolina Market Climate Change

Was this article valuable?

Here are more articles you may enjoy.

Insurers Must Defend Hotels Accused of Sex Trafficking of Minors

Insurers Must Defend Hotels Accused of Sex Trafficking of Minors  eBay Settles Couple’s Harassment, Stalking Claims for $55.7 Million

eBay Settles Couple’s Harassment, Stalking Claims for $55.7 Million  Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver

Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver  Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks

Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks