Leading U.S. insurers have nearly half-a-trillion dollars invested the fossil fuel energy and the electric and gas utility sectors, according to a report out today that urges state insurance regulators and board members of these companies to help move them out of such investments.

The winds continue to shift toward more regulation of insurance industry investments where it concerns climate change following transitions out of coal and other similar energies by European insurers and pushes by some state regulators to drive insurers away from investing in so-called “dirty energy.”

A report out from Ceres, a Boston, Mass.-based nonprofit group that advocates for sustainability leadership, details insurer investments in sectors the group said have become increasingly risky as prices and demand drops and the world’s governments continue mobilizing to reduce reliance on fossil fuels.

The report, “Assets Or Liabilities? Fossil Fuel investments of Leading U.S. insurers,” uses information including U.S. insurers’ year-end 2014 statutory financial statements to look at 40 large U.S. insurance groups.

“Cumulatively, the insurance groups analyzed owned investments of nearly a half-trillion dollars ($459 billion) in oil and gas, coal, and electric/gas utilities at the end of 2014 — an amount roughly equal to the GDP of Norway,” the report states.

The report was presented in a morning conference call with Ceres, California Insurance Commissioner Dave Jones, a representative from consulting firm Mercer, which assisted with the report, and a financial analyst from Barclays Investment Bank. Barclays provided baseline investment comparisons used in the report.

Jones, who is vice chair of the National Association of Insurance Commissioners Climate Change and Global Warming Working Group, called for regulation similar to what he has sought in California.

California Data Call

Jones in January asked all insurance companies doing business in California to voluntarily divest from their investments in thermal coal. The request followed an announcement by Jones last year that he plans initiate a data call that requires insurance companies to annually disclose their carbon-based investments.

On Tuesday’s call Jones offered a reason for his moves, which echoes the reasoning the authors of the report give for their call to action: insurers are at risk of having their investments stranded as these energy sectors lose money and continue to fall out of favor in the public eye.

“I took these steps because of the concern that I have as an insurance regulator that the oil, coal and gas assets will become stranded assets on the books of insurance companies,” Jones said.

The Ceres report calls on board of director members of these companies to step in.

“Boards should consider requiring the insurers’ Investment Policy Statements (IPS) to explicitly include a carbon asset or climate change risk management strategy, which the board would review on a regular basis,” the report states.

The authors also seek action by the NAIC, suggesting state regulators employ the NAIC’s risk-based capital requirements.

“In light of prospective risk considerations related to carbon-intensive assets, state insurance regulators should consider enhancements to the risk-based capital (RBC) formula to include fossil fuel sector concentration risk,” the report states. “It is noted that the RBC formula is already quite detailed as it pertains to investment risks, however fossil fuel concentration risk is not included.”

The NAIC has for several years poked into how insurer investments may be impacted by climate change through a risk disclosure survey that has been used in the past to criticize the industry for a lack of preparedness in addressing climate-related risks and opportunities.

Finally, the Ceres report also calls on state insurance regulators to do their part.

Finally, the Ceres report also calls on state insurance regulators to do their part.

“Overall, state insurance regulators should consider directing the resources and expertise of the NAIC, especially its Capital Markets & Investments Analysis Office, to better understand how carbon asset risk might impact insurers’ credit risks and systemic/market risks,” the report states.

Momentum for pushing insurance companies out of certain investments has been building for some time.

Jones’ coal divestment call earlier this year followed footsteps laid down by a few European insurers, including an announcement a year ago by Henri de Castries, chairman and CEO of French insurer AXA, that the company was ridding itself of investments in companies most exposed to coal-related activities.

Volatility

Investments in some energy sectors outlined in the report have experienced volatility lately, and because of goals set last year in Paris at the COP21 UN climate summit to reduce carbon emissions and keep global warming to 2 degrees Celsius those sectors may fare even worse, according to the report’s authors.

“During the past eighteen months, oil price volatility and related fossil fuel company losses negatively impacted investment results for some insurance companies,” the report states.

The report shows that between 2012 and 2015, broad market index returns have exceeded returns for the fossil fuel sector overall.

The report also compares the MSCI ACWI index, which encompasses 2,450 companies with a market capitalization of $34.5 trillion, with the MSCI ex-Fossil Fuels index that “clearly shows investments in fossil fuels lagging the overall market over this time period.”

Broad Push

The push to get out of these investments extends beyond the insurance industry to the entire financial industry.

Mark Carney, the governor of the Bank of England and the chair of the G20 Financial Stability Board, in a September 2015 speech at Lloyd’s of London issued a strong warning to insurers and the financial services industry about the risk posed by carbon investments.

Carney said a reduction in burning fossil fuels as outlined by the Intergovernmental Panel on Climate Change to limit global temperature rises to 2 degrees above pre-industrial levels would render the vast majority of oil, gas and coal reserves “literally unburnable without expensive carbon capture technology, which itself alters fossil fuel economics.”

The Financial Stability Board announced in December 2015 created an industry-led disclosure task force on climate-related financial risks with former New York Mayor Michael Bloomberg as chair. The voluntary climate-related financial risk disclosures would provide information to lenders, insurers, investors and other stakeholders, according to the board.

Mark Lewis, managing director OF European Utilities Research for Barclays, said during the conference call on Tuesday that analysis suggests capping carbon emissions en route to the achieving the 2-degree goal sought in the Paris Agreement would reduce the revenues of the upstream fossil-fuel industry globally by a cumulative $33 trillion by 2040.

“This number is simply too big for investors to ignore and should galvanize investor engagement with fossil fuel companies on the risk of stranded assets,” Lewis said.

Hartwig Critical

Not everyone thinks more oversight of insurer investments as suggested in the report is wise.

“They would probably invite added regulation, but even beyond that they are trying to impose their own view of the world on the insurance industry’s investment portfolio,” said Robert Hartwig, an economist and president of the Insurance Information Institute. “The entire Ceres investment report is a solution in search of a problem.”

Hartwig said he’s not disputing the veracity of climate change, but he is disputing that “insurers are somehow unaware of their investments.”

Energy investments are a small part of the “insurance industry’s vast and extremely well-diversified portfolio,” he added.

More importantly, replacing these investments with investments in things like green energy – which he noted does not have a stellar record of returns – could cause insurers to lose money, leaving them with one alternative, he said.

“What Ceres will not tell you is that if carbon-based energy exposure is removed from the industry’s portfolio, overall this will likely result in reduced portfolio performance and this would necessarily require higher rates for all types of life insurance and property/casualty insurance,” Hartwig said. “Ceres should ask the public if they are willing to pay higher insurance premiums permanently across the board based on their recommendations. Because that is the only possible outcome.”

Hartwig acknowledged fossil fuels can be a volatile investment, but historically they provide good returns and dividends, while green energy investments have no proven track record.

Hartwig also downplayed any perceived dangers of insurers getting into financial distress or becoming insolvent because of bad investments or catastrophic weather events.

“The proportion of insurers that become insolvent is a tiny fraction of 1 percent in any given year,” he said. “It’s very rare and usually it has nothing to do with expenses due to catastrophes.”

Abrupt Shift

Dave Snyder, vice president of international policy for the Property Casualty Insurers Association of America, warned against any abrupt shifts in the way insurers handle their investments or are required to handle them.

“Ceres is, after all, an advocacy group with a point of view which they regularly put forward,” Snyder said. “Our role is different. Our role is to take in data from all sources and to make our best judgement on investments. Insurers need to be very deliberate about what they do and not act prematurely, nor should they act monolithically.”

Snyder believes there could be broader risk if insurers all begin investing in the same way.

The P/C industry is capitalized “at historically high levels,” and it is an industry characterized by competition and various business models, he said, adding these are “strengths and should not be cut.”

Jim Jones, executive director for the Katie School of Insurance and Financial Services, at Illinois State University, who recently spoke to a group of Berkshire Hathaway investors about climate change, believes that politics is the biggest obstruction to any fact-based conversation between groups like Ceres and those who think what the group is trying to do is a bad idea.

“What I find frustrating is that we can’t seem to have intelligent conversations about climate change in the same way we do with other trends potentially affecting the industry,” Jones said. “For example the industry is looking at the impact of driverless cars – a topic at nearly every insurance industry conference now despite the fact that they hardly exist and it takes decades to turn over the U.S. fleet even if they were available today. Yet the impact of driverless cars, as significant as it could be, is going to be a lot less than climate change.”

The argument that insurers only write one-year policies so if things get bad because of climate change they can just withdraw from the market must be followed up with answers about how that business would be replaced, how it would affect commissions and recruitment of producers, and the length of time it would take to withdraw from a market – or multiple markets – affected by climate change, he said.

“It’s just time to be looking at this and analyzing how all of this is interrelated,” Jones said. “I’m glad that the rating agencies and regulators are looking at it, otherwise it doesn’t happen.”

State Farm

The report zeroes in on several insurers for investments in gas and oil, one of which is State Farm.

While State Farm doesn’t have a high percentage of its investments in oil and gas, it has a great deal of money in those sectors, particularly in the form of direct investments, which is unlike many other insurers on the list whose investments were largely in the form of bonds, according to the report.

“State Farm is very unusual for insurance companies in that it has a lot of its oil and gas investments in direct holdings, or equity,” said Cynthia McHale, director of the Ceres insurance program. “They’ve chosen a different strategy, which is direct investment.”

She said that State Farm’s direct investment is “by far bigger than any of the 40 insurance groups we looked at.”

Ceres found that as of Dec. 31, 2015, State farm held 37 million shares of Exxon Mobil Corp. stock, and more than 16 million shares in Chevron Corp.

Exxon is State Farm’s third largest direct investment behind Disney, and Johnson and Johnson, according to Ceres.

“They are really going in big for Exxon Mobil,” McHale said.

Standard & Poor’s in April stripped Exxon of its highest AAA measure of credit-worthiness, cutting it to AA+. Until the rating was cut, Exxon had maintained its AAA rating since the Great Depression.

Angela Thorpe, a State Farm spokeswoman, replied to a request for comment with a written statement:

“State Farm is certainly aware of the public policy interest in climate change. State Farm investment decisions are made in the best interests of our customers. We do not, however, discuss our investment strategies in a public forum.”

This isn’t the first time State Farm has run afoul of environmental interests.

A State Farm executive came under fire from activists for his position on the board of what some consider to be a “climate denier” group. Sierra Club, a progressive investor group and other activist organizations, have waged a years-long attrition campaign to force corporate participants to leave the American Legislative Exchange Council, a nonprofit comprised of conservative state lawmakers and members of the private sector that drafts model legislation and focuses its lobbying on a state-by-state basis.

Groups opposed to ALEC say its philosophies and actions have consistently opposed efforts to combat climate change.

State Farm is represented on ALEC’s private enterprise council by counsel Roland Spies. Exxon has also been tied to the ALEC board.

Insurer Ranking

The Ceres report breaks down insurer investments in several sectors, but notably de-emphasizes insurer investments in coal because coal investments have become an increasingly small portion of the 40 insurance groups’ bond and equity holdings as the market value of U.S. coal companies has fallen.

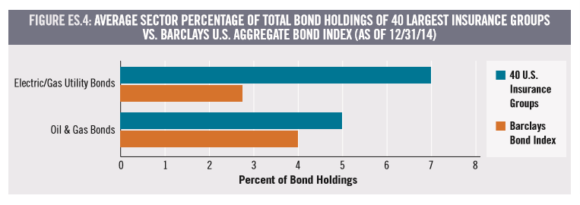

Certain insurance groups owned double the median bond portfolio concentration in the oil and gas sector as measured by Barclays U.S. Aggregate Bond Index.

The report lists the biggest investors by percentage in gas an oil and notes that the following 12 carriers were the biggest investors in those sectors in terms of percentage of their total bond portfolios (figures are in millions):

- Ameriprise – $25,023 – 12.4%

- Lincoln National – $84,999 – 11.8%

- Voya Financial – $80,127 – 10.9%

- Northwestern Mutual – $137,491 – 9.9%

- Allianz – $88,824 – 9.3%

- Jackson National – $50,990 – 8.9%

- John Hancock – $70,028 – 8.8%

- Allstate – $58,792 – 8.2%

- Nationwide – $60,625 – 8.2%

- Pacific Life – $35,998 – 8.0%

- Genworth – $50,004 – 7.8%

- USAA – $37,927 – 7.8%

Representatives for all the above were contacted for comment.

Maryellen Thielen, a spokeswoman in Allstate corporate relations, provided the following statement:

“In its nearly $80 billion portfolio, Allstate holds diversified energy investments that range from producers to regulated utilities, including investments in solar, wind and geothermal. Most of our holdings are investment grade corporate bonds with historically low default rates. As a core part of our investment management and risk/return evaluation process, we continually evaluate prevailing and potential future market conditions, regulations and investment creditworthiness, among other factors, and adjust our portfolio accordingly.”

The statement said the insurer manages these assets “proactively” to support Allstate’s claims-paying abilities to provide financial security to its policyholders through its life insurance and annuity products.

Holly C. Fair, director of corporate communications for Lincoln Financial Group, also provided an official comment:

“The report reflects data as of year-end 2014, while we have reported numbers as of 1Q2016. Please visit the investor relations section of our website to review our 1Q2016 earnings call transcript, where we point to actions we have taken regarding our investment portfolio and energy exposure.”

Beth McGoldrick, assistant vice president of public relations for John Hancock Financial Services and Manulife Asset Management, part of John Handcock, offered the following statement:

“Manulife and John Hancock have a well-diversified, high quality investment portfolio with a blend of assets. Our investments in the energy sector, specifically, range across all types of energy, including significant investments in renewable energy. As a matter of policy, we conduct extensive due diligence on a wide range of factors, including potential regulatory changes, that could affect the returns generated by, and the fair market value of, all of our investments.”

According to the statement, as of the end of 2015, Manulife has invested $9.4 billion in renewable energy and energy efficiency projects, with investments including hydro, wind, geothermal, biomass and solar.

Earlier this month, John Hancock announced it was investing $227 million in a diversified portfolio of rooftop solar installments with Solar City that represents over 200 megawatts of generation capacity, and to date this year the company has invested roughly $1 billion in utilities and oil and gas and $360 million in renewables, according to the statement.

The rest of the insurance groups on the list declined to comment or did not respond to a request for comment.

There were also several carriers called out for having relatively few investments in oil and gas:

- ACE – $19,738 – 2.0%

- W.R. Berkley – $11,367 – 1.8%

- QBE – $2,272 – 1.5%

- Progressive – $14,101 – 0.2%

Representatives from these insurers did not respond to a request for comment.

Related:

- Sierra Club Dragging State Farm into Climate Change Battle

- Climate Change Easy Bet to Be Hot Topic at Insurance Regulators’ Meeting

- Berkshire Hathaway Balks at Reporting on Climate Change Risks

- How Will Paris Agreement Change The Insurance Industry?

- Insurers Stepping Toward Greater Green Investment Footprint

- AXA Plans to Sell Coal Assets, Citing Concerns About Climate Change

Ceres Assets Risk Fossil Fuel Insurers

Topics USA California Carriers Legislation Europe Energy Oil Gas Market Climate Change

Was this article valuable?

Here are more articles you may enjoy.

Viewpoint: Who Gets Credit for Successful Renewal During Soft Reinsurance Market?

Viewpoint: Who Gets Credit for Successful Renewal During Soft Reinsurance Market?  Brown & Brown Estimates Cost of Howden-Driven Talent War Could Hit $60M in 2026

Brown & Brown Estimates Cost of Howden-Driven Talent War Could Hit $60M in 2026  As US Residential Solar Industry Craters, Florida Bucks Trend

As US Residential Solar Industry Craters, Florida Bucks Trend